A financial services internal communications team operates under a double mandate that office-IC playbooks routinely ignore. Every message the team sends is simultaneously an engagement artifact (did it land, did it move behavior) and a compliance artifact (is there an audit trail, is there receipt evidence, was sensitive content scoped to the right audience). Both jobs have to be done, on the same send, on a stack that survives both employee-engagement scrutiny and regulatory examination.

The regulatory perimeter matters less than the structural truth. FINRA and the SEC define obligations for US broker-dealers and investment advisers. The OCC, FDIC, and Federal Reserve cover US banks. The FCA covers UK firms. OSFI covers Canadian federally regulated entities. MAS covers Singapore. The named rules differ across those regimes (FINRA Rule 3110 and 4511, SEC Rule 17a-4, FCA SYSC, OSFI Guideline B-10, MAS Notice 644), and the retention windows differ. The operational obligation rhymes across all of them: retain certain internal communications for years, produce them on demand, evidence delivery and acknowledgment for compliance-critical messages, and route distribution according to information barriers.

Internal communications in financial services is the practice of running an IC program that produces engagement outcomes (read, understand, act) and audit-grade evidence (who received, who acknowledged, when, on what device) from the same send. This is a 2026 playbook for the Director of Internal Communications at a regional bank, an asset manager, an insurer, or a broker-dealer running that program for real, and the argument is direct: a financial services IC program that serves one mandate and lets the other slip is a program waiting to either lose engagement credibility or fail an exam.

The double mandate of financial services IC: compliance and engagement, neither optional

Every internal message at a regulated employer is potentially subject to regulator inspection. That changes the design constraints of the IC program, not just the content of the messages.

On the compliance side, the obligations are specific. FINRA Rule 3110 requires supervision of internal communications. FINRA Rule 4511 sets a 6-year retention floor for many records. SEC Rule 17a-4 requires broker-dealers to retain certain communications for 3 years, with the first 2 years in an accessible form. FCA SYSC sets out similar supervisory and recordkeeping expectations in the UK. OSFI Guideline B-10 covers Canadian federally regulated entities. MAS Notice 644 covers Singapore. The IC team is not the compliance team, but the IC stack has to feed the firm's recordkeeping architecture, evidence delivery and acknowledgment for compliance-critical messages, and respect information barriers in audience design.

On the engagement side, financial services has every engagement problem the rest of the economy has, plus a set of overhangs the rest of the economy mostly does not. RTO mandates hit harder in trading-floor and customer-service roles where the policy is a return to 4 or 5 days in office rather than a 3-day hybrid baseline. AI displacement anxiety hit financial services first because the industry has the most automatable middle-office work (research support, KYC processing, compliance review, claims adjudication). Burnout is structural at the investment-banking end of the industry and increasingly structural at the retail-branch end. M&A consolidation produces a quarterly "another acquisition" rhythm that employees who have been through three mergers in five years read with structural skepticism.

The trap most IC teams fall into is defaulting to one mandate and letting the other slip. Compliance-first programs become legal newsletters nobody reads, which then fail the engagement side of the program review. Engagement-first programs produce read-but-not-acknowledged content the compliance team finds out about at the next exam. Neither version of the program is defensible. The 2026 version of financial services IC serves both mandates at once, by designing the channel, the audience, and the measurement system to produce engagement and audit evidence from the same send.

Why generic IC tools fail in banks, asset managers, and insurers

The diagnostic work of financial services IC sits in three structural failure modes that generic IC tools (and generic IC playbooks) hit in a regulated environment.

Audit trails and message retention requirements

When a regulator asks for the firm's internal communications from a specific date range to a specific audience, the comms team has to produce them in a documented, time-stamped, immutable form. Open rate data is not an audit trail. It is a marketing metric.

The common failure mode is a comms team running on a generic newsletter tool or a vanilla Outlook distribution list that produces marketing-style analytics but no per-recipient delivery confirmation, no immutable record of the message body as sent, and no retention beyond 90 days. The compliance team learns about the gap when an exam request lands and the IC team realizes the records they need to produce are not being captured anywhere.

The fix is a stack where the IC tool integrates with the firm's record-retention system (Smarsh, Global Relay, Microsoft Purview, or whichever dedicated archiving tool the firm runs). Every send is captured automatically. Retention happens by default rather than by exception. The IC team's job is not to become the system of record; it is to feed the system of record cleanly. The internal communications job description at a regulated employer carries this audit responsibility on top of the standard role, and the job spec should reflect it.

Evidence of receipt (FINRA, SEC, and similar implications)

For policy attestations, code-of-conduct affirmations, material non-public information (MNPI) acknowledgments, and similar compliance-critical messages, regulators want evidence that the named employee actually received the message, opened it, and confirmed they read it. Per-recipient acknowledgment, time-stamped, attributable.

The common failure mode is a code-of-conduct refresh sent through a corporate distribution list with no acknowledgment mechanism. Six months later, the compliance team asks "who confirmed receipt?" and the IC team has the email open rate. The open rate is not the answer to that question.

The fix is an IC platform with employee-level acknowledgment receipts stored against the employee record and exportable to the firm's compliance system on request. This is one of the specific compliance jobs Cerkl Broadcast supports, and naming the capability honestly is what earns the trust to recommend it. Cerkl is the IC layer, not a compliance product. The acknowledgment data Cerkl produces feeds the compliance team's record. The compliance team owns the determination; the IC team owns the delivery and the receipt evidence.

Segregation of duties and need-to-know distribution

Financial services internal comms has to respect information barriers. The trading desk does not receive deal-team communications from investment banking. Retail-branch staff do not receive research notes embargoed for institutional clients. The audience tool has to mirror the firm's information-barrier architecture.

The common failure mode is a corporate-wide distribution list that bypasses information barriers because the comms team did not realize the list spanned two restricted populations. A pending-deal note hits the retail floor. A research embargo gets broken by a routine internal newsletter. The compliance event that follows is one of the more uncomfortable conversations an IC director can have.

The fix is dynamic audience segmentation pulled from HRIS and the firm's identity system, with role, team, and jurisdiction attributes that mirror the firm's information-barrier topology. The same segmentation that drives compliance-correct distribution also drives engagement-correct personalization, which is why this layer is worth getting right early.

The compliance side: what regulators expect from internal communications

The operational compliance arc covers four specific things a 2026 financial services IC program has to produce on demand. The IC platform does not have to do all four jobs itself; it does have to participate in an architecture that does.

The first is audit logs and immutable records. Every send captured in a time-stamped, tamper-evident record. The IC platform does not have to be the system of record (that is the surveillance and retention tool's job), but the integration has to be clean and automatic rather than a manual export workflow that breaks the first time someone goes on vacation. A weekly CSV export the comms manager runs by hand is a control with a single point of failure.

The second is retention. SEC Rule 17a-4 requires broker-dealers to retain certain communications for 3 years, with the first 2 years in an accessible format. FINRA Rule 4511 extends to 6 years for some categories. Some firm policies extend further out of caution, particularly for messages tied to ongoing litigation or regulatory inquiry. The IC team's job is to design the program so retention happens by default and the firm does not need to reconstruct records under deadline pressure when an exam request lands.

The third is evidence of delivery and read-receipt at the recipient level. Per-employee acknowledgment data, time-stamped and attributable. This is the deliverable when the compliance team or an external auditor asks "did employee X receive the new code of conduct, and did they acknowledge it?" The IC platform needs to support that question with data, not with a synthesized report assembled after the fact.

The fourth is sensitive-information handling. Material non-public information, customer-confidential data, deal-related information. The audience tool has to respect information barriers, which is the segregation-of-duties failure mode above in operational form. The platform also has to handle restricted distribution at the message level: a partner update that goes only to managing directors, a research note that respects embargo timing, a layoff communication that has to reach affected employees before it reaches the rest of the firm. None of those scenarios are exotic. All of them happen monthly at a real financial services firm.

The architecture that handles those four jobs is not a single tool. It is an IC platform feeding a surveillance and retention system, with dynamic segmentation tied to compliance-relevant employee attributes, and acknowledgment receipts as a first-class output rather than an afterthought. A program that runs on that architecture holds up under examination. A program that runs on a generic newsletter tool with manual exports does not.

The engagement side: what financial services employees need from IC in 2026

Compliance is half the mandate. The engagement half is harder for most IC teams because it is the half their leadership measures them on monthly, while the compliance half only surfaces during an exam.

Financial services employees in 2026 are reading internal communications under four engagement realities that are sharper in this industry than in most others.

The first is return-to-office tension. Major banks have run 4-day and 5-day RTO mandates by 2026; asset managers have run 3-day hybrid baselines. The IC team is communicating policies a meaningful share of the workforce disagrees with, sometimes loudly. Tone-deaf "back to the office for connection!" messaging makes the comms team part of the problem rather than the messenger. The teams that name the tradeoff openly (productivity gains the firm is targeting, flexibility losses employees are absorbing, the rationale leadership is acting on) earn more trust than the teams that pretend the policy is uncontroversial.

The second is AI displacement anxiety. Financial services is one of the most-exposed industries to AI-driven middle-office automation. Research support, compliance review, KYC processing, claims adjudication: all heavily affected. Employees know this; the trade press covers it constantly. IC messages about the firm's AI strategy that ignore the displacement concern read as dishonest. Messages that name the tradeoffs (which roles are most exposed, what the firm is investing in to reskill, what the timeline is) land better than messages that pretend there are no tradeoffs.

The third is burnout and retention. Investment banking burnout is the canonical case, with associates and analysts working hours that make most other industries look gentle. Insurance and retail-banking branch staff carry their own version, with high-friction customer interactions and pay structures that have not tracked inflation. The IC program is communicating wellbeing benefits to a workforce that, on the data, mostly is not using them. Receipt evidence (employees acknowledged the benefits message) is not the same as engagement evidence (employees actually used the benefit). Both need to be measured and the gap between them named.

The fourth is M&A fatigue. Financial services consolidates faster than any other industry except technology. For most financial services IC teams, "another acquisition announcement" is a quarterly artifact. Employees who have been through three mergers in five years read those messages with structural skepticism because they have learned the pattern. The IC team that acknowledges that pattern openly, addresses the implications for the affected employees by name, and avoids the templated "stronger together" framing earns more trust than the team that runs the boilerplate every time.

A communications architecture that handles both: audience segmentation, channel-preference handling, audit-grade record-keeping

A financial services IC architecture that serves both mandates without forcing the team to run two separate programs has four components. Each is doing engagement work and compliance work at the same time.

The first is dynamic audience segmentation pulled from HRIS and the firm's identity provider. Audiences that update automatically as employees move between desks, teams, and jurisdictions. Segmentation that mirrors the firm's information-barrier topology so compliance-correct distribution and engagement-correct personalization come from the same source rather than from two different systems that fall out of sync.

The second is channel-preference handling. A trader's preferred channel is not the same as a retail-branch employee's preferred channel, which is not the same as a back-office analyst's preferred channel. The IC platform has to handle email plus mobile plus (where the firm has invested) Microsoft Teams, SharePoint, or in-app surfaces without forcing a single channel on a workforce that uses many. Single-channel programs at multi-channel employers underperform in both directions: they miss engagement on the channels they do not run, and they generate audit gaps on the channels they do not cover.

The third is audit-grade record-keeping. Every send stored as an immutable record. Every receipt logged at the employee level. Integration with the firm's surveillance and retention tools so the IC platform feeds the system of record rather than replacing it. The integration is the design decision that matters: a clean automatic feed versus a manual export workflow is the difference between a program that holds up under exam pressure and a program that breaks the first time it gets one.

The fourth is receipt evidence on the same send. The same send that drives engagement (employees read, click, take action) also produces the acknowledgment record compliance needs. One send, two outputs. Engagement reporting and compliance reporting come from the same source data rather than from two separate captures the IC team has to reconcile manually.

Cerkl Broadcast is built to handle the IC layer of this architecture: HRIS-fed audience sync, segmentation that maps to information barriers, send infrastructure across email and mobile and SharePoint and Teams, engagement analytics, and acknowledgment receipts at the employee level. Dedicated surveillance and record-retention tools (Smarsh, Global Relay, Microsoft Purview) handle the systems-of-record layer. The right design integrates the two; the wrong design picks one and pretends it covers both jobs. The honest pitch on Cerkl is the architecture pitch: get the IC layer right and integrate it cleanly with the firm's existing surveillance stack.

Measurement for financial services IC: regulatory metrics plus engagement metrics together

Corporate IC measurement defaults to open rate. Financial services IC measurement has to default to three things at once because reporting only the engagement layer is what produces a program that looks healthy until the next exam.

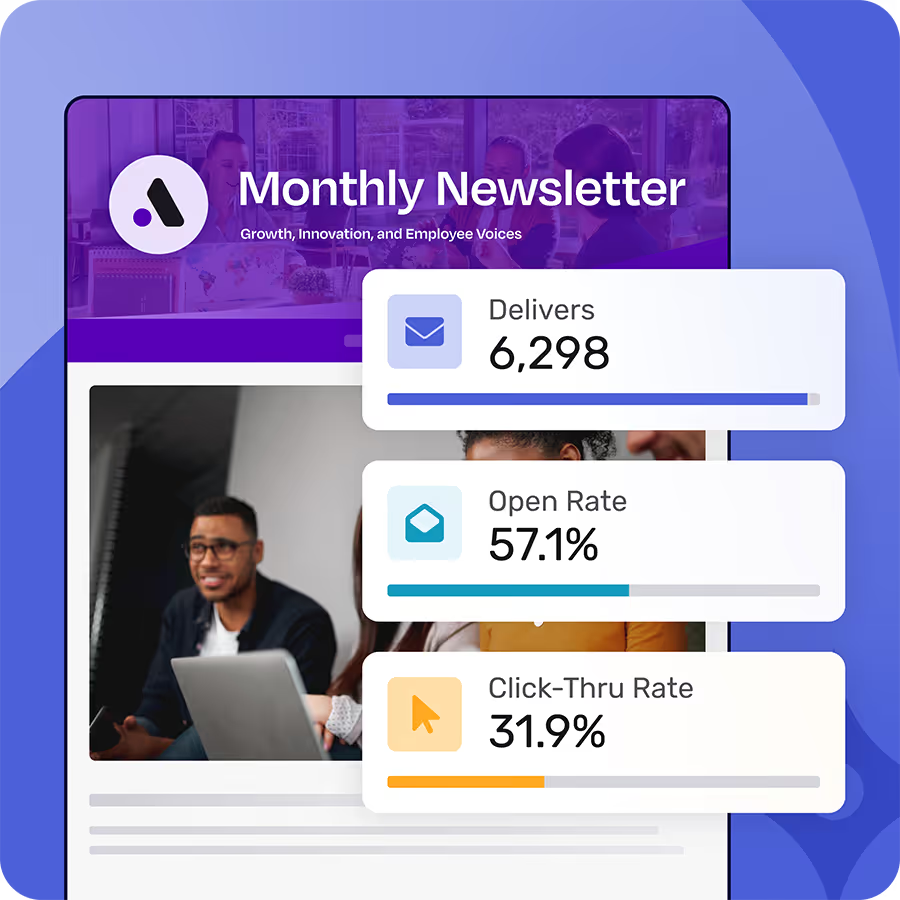

The first is engagement metrics. Open rate, click rate, read-through, action completion. The standard IC measurement layer, and the layer leadership is most familiar with. These metrics matter; they are not sufficient on their own.

The second is compliance metrics. Receipt evidence by recipient, acknowledgment completion rate for attestation messages, retention coverage as a percentage of sends captured in the system of record. The acknowledgment completion rate is the leading indicator the compliance team should be asking about. "We sent the new code of conduct to 4,000 employees and 3,200 acknowledged within 14 days" is a number that holds up under examination. The follow-up cadence to get the remaining 800 employees to acknowledgment is the operational discipline that makes the compliance side of the program work.

The third is audience-correctness metrics. Did the right audience receive the message? Were information-barrier restrictions respected on every send? Misroute rate (sends that reached an audience they should not have) is one of the few compliance numbers most IC platforms can produce automatically and most IC teams do not track. A misroute rate of zero is the target. A measured misroute rate that surfaces in the IC team's dashboard before it surfaces in a compliance incident is the operational evidence the architecture is working.

Cerkl Broadcast analytics ties engagement, compliance, and audience-correctness into one report so a comms leader walking into a quarterly review or an examination has a single source of truth rather than three separate dashboards to reconcile. A financial services IC program with no integrated measurement view is a program that has to manually assemble the answer to "how is this working?" every quarter, which is the moment a busy IC team can least afford to do that.

A 30-day plan to upgrade financial services internal communications

Most financial services IC leads are running an inherited program with known gaps and limited time to fix them. The next four weeks generate the data that funds the architecture upgrade and improves the current program at the same time.

Week 1 is the compliance gap audit. Pull the firm's record-retention policy from Compliance or Legal. Map it against what the current IC stack actually captures, send by send, audience by audience. The gap almost always shows the same pattern: receipt evidence is missing for attestation messages, retention coverage is partial, the integration with the firm's surveillance tool is manual or absent. That gap is the audit finding waiting to happen. Naming the gap before the regulator does is the first move. Document it in a one-page memo for the head of Compliance. Week one of the working relationship that funds the rest of the plan starts there.

Week 2 is the audience-architecture audit. Pull the audience definitions from the current IC tool. Check them against the firm's information-barrier map, which Compliance owns. The mismatches are concrete: corporate-wide lists that span restricted populations, distribution groups that do not update when people move desks, audience segments that exist in the IC tool but no longer reflect the firm's current org chart. The cleanup list at the end of the week is the priority queue for the next quarter. The audit alone often produces three or four immediate fixes worth making before any new platform decision.

Week 3 is the receipt-evidence pilot. Pick a single policy attestation that is due in the next 30 days (code of conduct refresh, gift policy update, MNPI training reminder, annual compliance attestation). Send it through an IC platform with employee-level acknowledgment receipts. Measure send-to-acknowledgment time, acknowledgment completion rate by team, and the follow-up cadence required to push the laggard cohort to 100 percent. Cerkl Foundations is the no-procurement entry point for the pilot: a regional bank or asset manager can run it at one department without a sales cycle, which keeps the pilot small and the data clean.

Week 4 is the architecture brief. Combine the Week 1 compliance gap, the Week 2 audience errors, and the Week 3 acknowledgment data into a one-page memo. The argument is direct: today's program serves engagement; the 2026 program serves engagement and compliance from the same send. The Week 3 pilot is the proof-of-concept. The Week 1 gap is the risk position. The Week 2 errors are the operational cleanup. The memo lands with the head of Compliance, the head of HR, and the head of IT in the same week, which is the only way the architecture upgrade gets prioritized against everything else competing for budget.

A financial services IC team that runs this four-week sequence ends the month with three things it did not have at the start: a documented compliance gap, a clean audience map, and a defensible acknowledgment pilot. Those three artifacts are the difference between a program that argues for resources from intuition and a program that argues for resources from data.

When Foundations is the right starting point for a financial services IC team (and when you'll need to grow into Omni AI)

Honest fit matters more than commercial pressure in this section, because the wrong product call on either side burns the IC team's credibility with their internal stakeholders.

Foundations is the right starting point for smaller regional banks, registered investment advisers, asset managers in the 100 to 1,000-employee range, insurance brokerages, and fintech firms that have a compliance posture but not a 5,000-employee multi-jurisdiction footprint. The free tier handles the IC layer of the compliance architecture cleanly: HRIS-fed audience segmentation, send infrastructure, engagement analytics, and receipt evidence. The team can integrate it with whichever surveillance and retention tool the firm already runs. There is no procurement cycle to start, which means the architecture upgrade conversation can start from a working pilot rather than from a vendor pitch.

Omni AI is the upgrade path for larger banks, multi-jurisdiction insurers, and global asset managers with deskless, branch, trading-floor, and advisor populations spread across channels. Email plus mobile plus Teams plus SharePoint plus in-app at scale. The engagement side gets more complex (more audiences, more channels, more personalization). The compliance side gets more complex (more jurisdictions, more recordkeeping requirements, more information-barrier topology). The architecture has to handle both at higher scale, which is the job Omni AI is built for.

The line between the two is not headcount alone. It is channel complexity. A 500-employee asset manager that runs everything through email and a single intranet sits comfortably in Foundations. A 2,000-employee regional bank with a deskless branch network and a separate corporate office runs into the Foundations ceiling. Naming where the firm actually sits on that line, honestly, is the IC director's job, not the vendor's.

Internal communications in financial services is a discipline defined by the double mandate. Engagement and compliance, on the same send, on a stack that survives both. A financial services IC team that designs the program for engagement only is a team waiting for an exam finding; a team that designs for compliance only is a team whose program nobody reads. The 2026 playbook is one program that does both jobs at once, on an architecture built around audience integrity, receipt evidence, and channel-correct delivery. The IC teams that build that program are the ones whose work holds up when the regulator visits and when the engagement survey lands.

FAQ

What is internal communications in financial services?

Internal communications in financial services is the practice of running an IC program that produces engagement outcomes (read, understand, act) and audit-grade evidence (who received, who acknowledged, when, on what device) simultaneously, on a stack that survives both employee-engagement scrutiny and regulatory examination. The defining constraint is the double mandate: every internal message at a regulated employer is potentially subject to regulator inspection, so the IC program has to design for compliance evidence and engagement outcomes from the same send.

What regulations affect internal communications in banks and financial services firms?

In the US, FINRA Rules 3110 and 4511, SEC Rule 17a-4, and similar rules cover internal communications supervision, retention, and recordkeeping for broker-dealers and investment advisers. The FCA SYSC sourcebook covers UK firms. OSFI Guideline B-10 covers Canadian federally regulated entities. MAS Notice 644 covers Singapore. The specific frameworks differ, but the operational obligations rhyme: retain certain internal communications for 3 to 7 years, produce them on demand to regulators, evidence delivery and acknowledgment for compliance-critical messages, and route distribution according to information barriers.

How is compliance-driven internal communication different from regular employee communication?

Regular employee communication optimizes for engagement (open rate, click rate, action completion). Compliance-driven internal communication has to deliver engagement and produce a documentary record at the same time: per-recipient acknowledgment, time-stamped delivery, immutable storage, retention through the regulatory window, and audience-correct routing that respects information barriers. The send mechanic looks similar; the architecture behind it (audit logs, retention integration, acknowledgment receipts, dynamic segmentation tied to compliance-relevant attributes) is substantially different.

What metrics matter most for financial services internal communications?

Three measurements together: engagement metrics (open rate, click rate, read-through, action), compliance metrics (receipt-evidence completion by recipient, acknowledgment rate for attestation messages, retention coverage of sends), and audience-correctness metrics (did the right audience receive the message, were information-barrier restrictions respected, misroute rate). The trap is reporting engagement alone and producing a program that looks healthy until the next regulatory examination, when the compliance numbers come up short.